VAT management

A number of Value Added Tax (VAT) schemes are operated by Her Majesty’s Revenue & Customs (HMRC). Additionally, businesses or organisations such as retailers, charities, etc., can have specific requirements related to VAT.

The VAT status of the organisation should be established at an early point in project scoping because this can affect the configuration of VAT within Sage X3. You must run VAT reports defaulted to the BRI legislation.

VAT submissions or Tax returns to HMRC must be made electronically via a system known as Making Tax Digital (MTD).

It is important to have a working understanding of these functions. Refer to the online help for details.

-

Tax level (GESTVI)

-

Tax determination (GESTVC)

-

Tax rates (GESTVT)

-

Accounts (GESGAC)

-

VAT entities (GESVATGRP)

-

Entry type groups (GESGTEGRP)

-

VAT boxes (GESVTB)

-

VAT form (GESVEF)

-

VAT returns (GESVFE)

UK VAT overview

VAT is charged on most goods and services that VAT registered businesses provide in the UK. VAT is also charged on goods and some services that are imported to the UK. When VAT registered businesses purchase goods or services, they can generally reclaim the VAT they have paid.

-

A VAT registered business must record the amount of VAT that they have charged on all goods or services they have sold. This is known as an output tax.

-

A VAT registered business must record the amount of VAT they have been charged on all goods or services that the business has purchased. This is known as an input tax.

-

A VAT registered business must show the VAT being charged for goods or services on all invoices they produce.

At the end of each tax period, normally every three months, the total output tax collected by the business is paid to HMRC. At the same time the total input tax paid out by the business is reclaimed for HMRC. This process is called the tax return.

For the 2020 tax year, three tax rates are applied in the UK:

|

Rate |

% |

|---|---|

|

Standard rate |

20% |

|

Reduced rate |

5% |

|

Zero |

0% |

Some goods and services can be classified as exempt or outside the scope of VAT.

UK VAT regulations require that VAT be calculated on the discounted amount of the invoice.

All businesses with a turnover (total income) of greater than 85,000 GBP must register for VAT. Registration is optional below this threshold.

VAT must usually be declared based on the invoice; however, cash VAT is allowed for small businesses. In this case, the triggering event is the payment of the invoice.

For certain categories of goods, for example mobile phones, and transaction amounts greater than 5000 GBP, reverse charge VAT will apply. In a reverse charge VAT transaction, the buyer pays HMRC the VAT directly. The invoices must clearly state that the transaction is subjected to reverse charge VAT and the buyer is responsible for payment to HMRC. The seller must record the VAT as an input tax and the output tax can be recorded in a contra account so there is no tax liability to HMRC.

VAT returns can be submitted as a single company or as a group of companies. See VAT entities.

All VAT registered businesses must submit their VAT returns online (MTD) and pay electronically. In some circumstances manual submission is permitted but this is rare: MTD enforces a digital link between the transactions and the VAT return up to and inlcuding the submission.

Settings related to the VAT process

VAT returns are calculated from the main general ledger (GESGAS), on the basis of VAT codes. The main functions that participate in the tax determination are:

-

Accounting codes (GESCAC): Used to define the set of VAT accounts that are associated with each tax rate.

-

Accounts (GESGAC): Used to define the accounts needed to manage the different ledgers of the company. For the accounts of the main general ledger, tax characteristics must be defined (tax management and allocation rules, default tax code, etc.)

-

BP tax rule (GESTVB): Used to define the tax rules associated with each business partner (e.g., Domestic, Export, Import with PVA, Import without PVA, EU, …)

-

Document type (GESGTE): Used to determine if the document is an invoice or a payment (used to trigger the VAT on invoice or Cash VAT), or as criteria for the calculating VAT boxes.

-

Entry type groups (GESGTEGRP): Used to create an entry type group for a given legislation when setting up VAT declarations. In the VAT boxes function (GESVTB), you can use the entry group code for detail VAT boxes on a single line rather than entering multiple lines for detailed entry types. Entry type groups share the same tax code + tax management + tax allocation combination.

-

Tax determination (GESTVC): Used to define, by crossing the tax rule (linked to BPs) and the tax level (linked to products), the tax rate to be used in sale and purchase invoices.

-

Tax rates (GESTVT): Used to define the codes for tax rates that can be applied to sale, purchase and A/P-A/R invoices, and related journal entries. Each tax rate code is associated with a set of VAT accounts based on its associated accounting code.

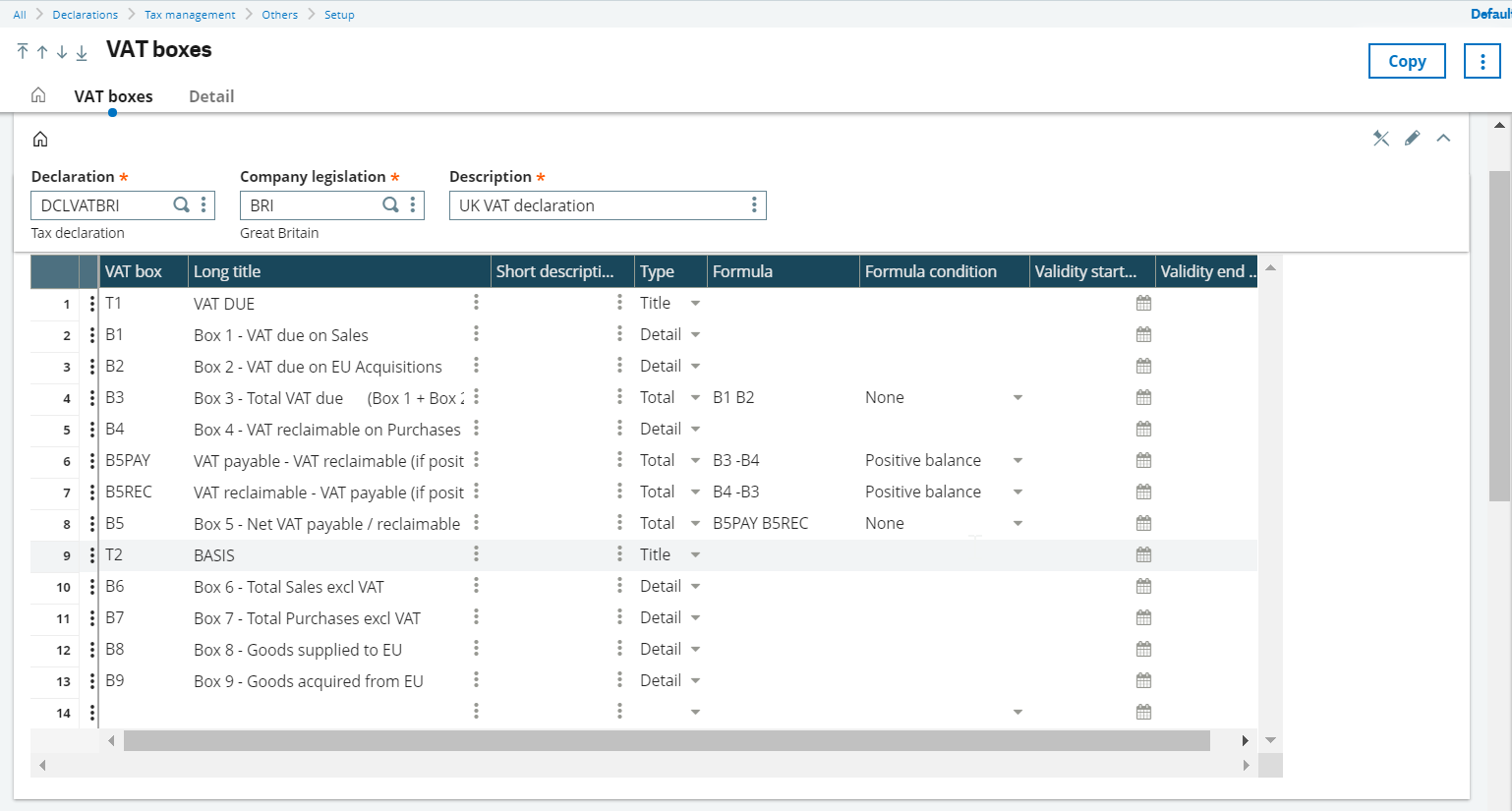

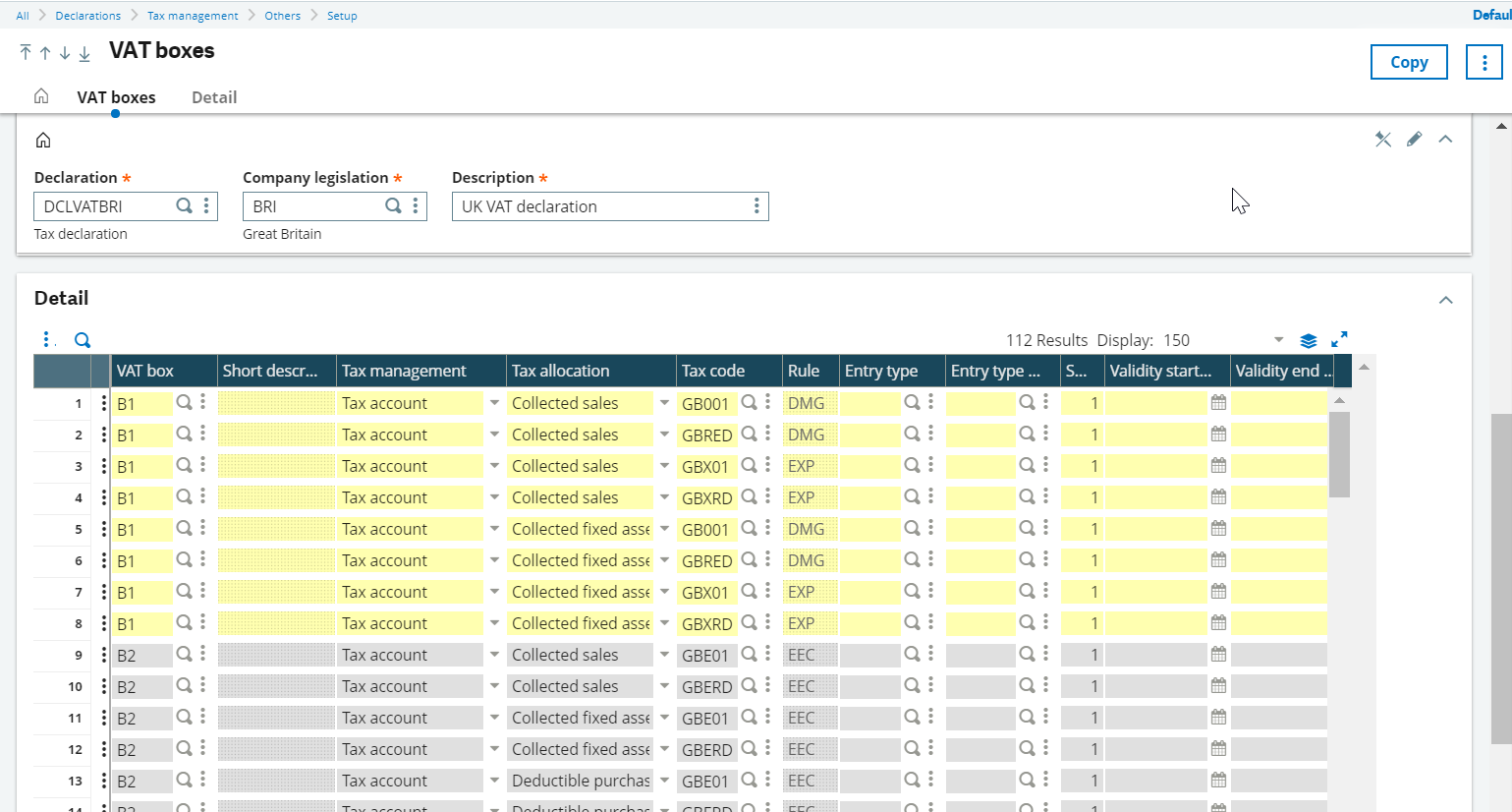

VAT boxes set-up (GESVTB)

Open: DECLARATIONS > Tax management > Others > Setup > VAT boxes

You use this function to define how VAT boxes are calculated. The first table defines the 9 VAT boxes required for UK VAT returns.

The second table defines the population rules for the 9 boxes, depending on the general ledger and the settings related to the account, the journal entry type and the VAT code.

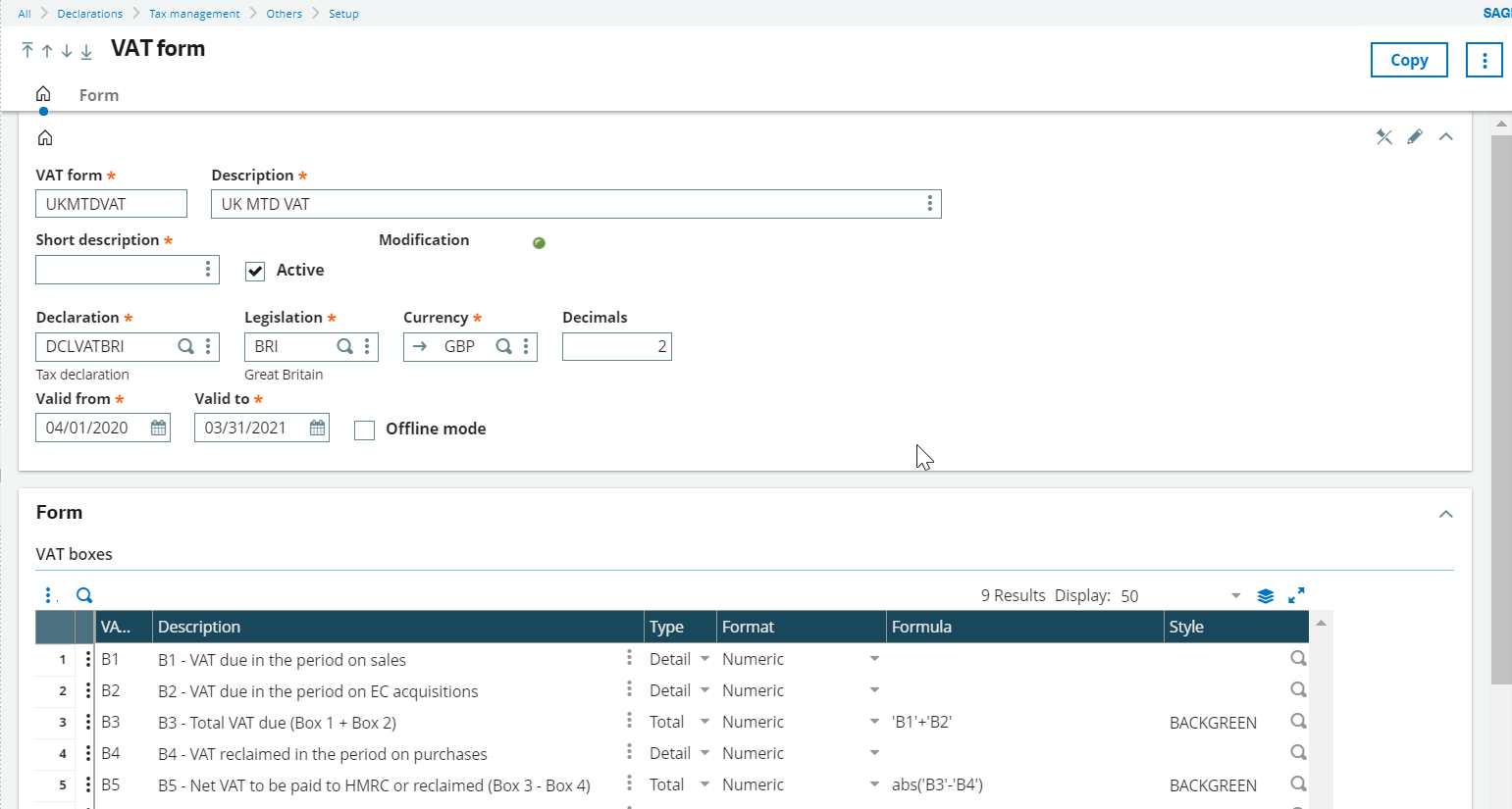

VAT form set-up (GESVEF)

Open: DECLARATIONS > Tax management > Others > Setup > VAT form

You use this function to set-up the structure of the VAT return.

When you set a form to offline mode, you can define specific VAT returns with no connection to HMRC. The VAT return period is not controlled, and you cannot submit the VAT returns. Offline mode is useful when initializing and testing the VAT process.

When a VAT form has been used for a VAT return, you can no longer modify the form. You can delete the VAT returns (possible under conditions) or you can create a new form.

VAT entities (GESVATGRP)

Open: DECLARATIONS > Tax management > Others > Setup > VAT Entities

Use this function to create and manage VAT entities for a single or multiple companies or a single or multiple sites. VAT entities enable you to define distinct VAT returns at the site level.

VAT returns are managed at the VAT entity level. You can define several processes, across sites, companies and groups. One common case is a company registered in multiple countries (EU).

VAT submission process

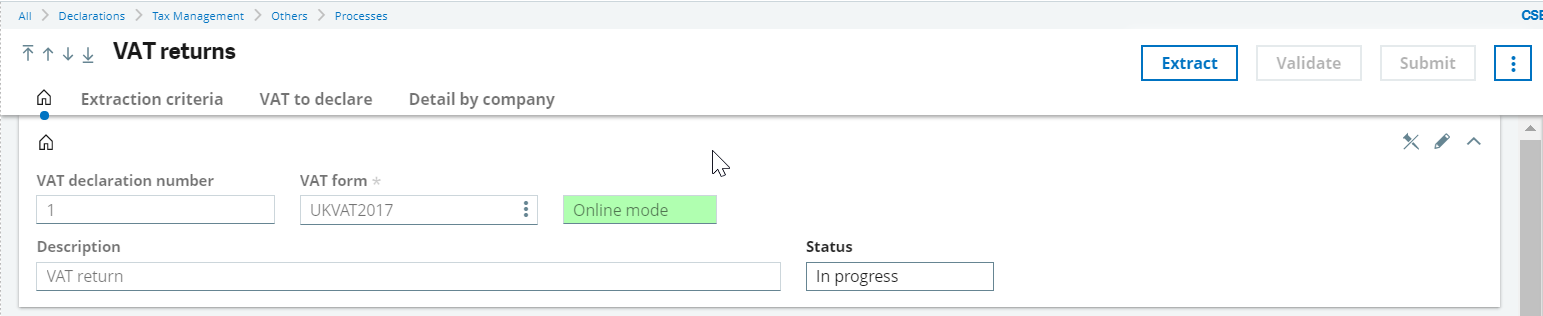

VAT returns (GESVFE)

Open: DECLARATIONS > Tax management > Others > Processes > VAT returns

Use this function to simulate, calculate, adjust, validate and submit the VAT returns regarding the British VAT entities you defined.

Because the VAT return period is controlled against HMRC and submitted digitally, you need HMRC credentials. You can use a VAT form in offline mode, but you cannot submit to HMRC with a form in this mode. This mode is useful for testing and initialization purposes.

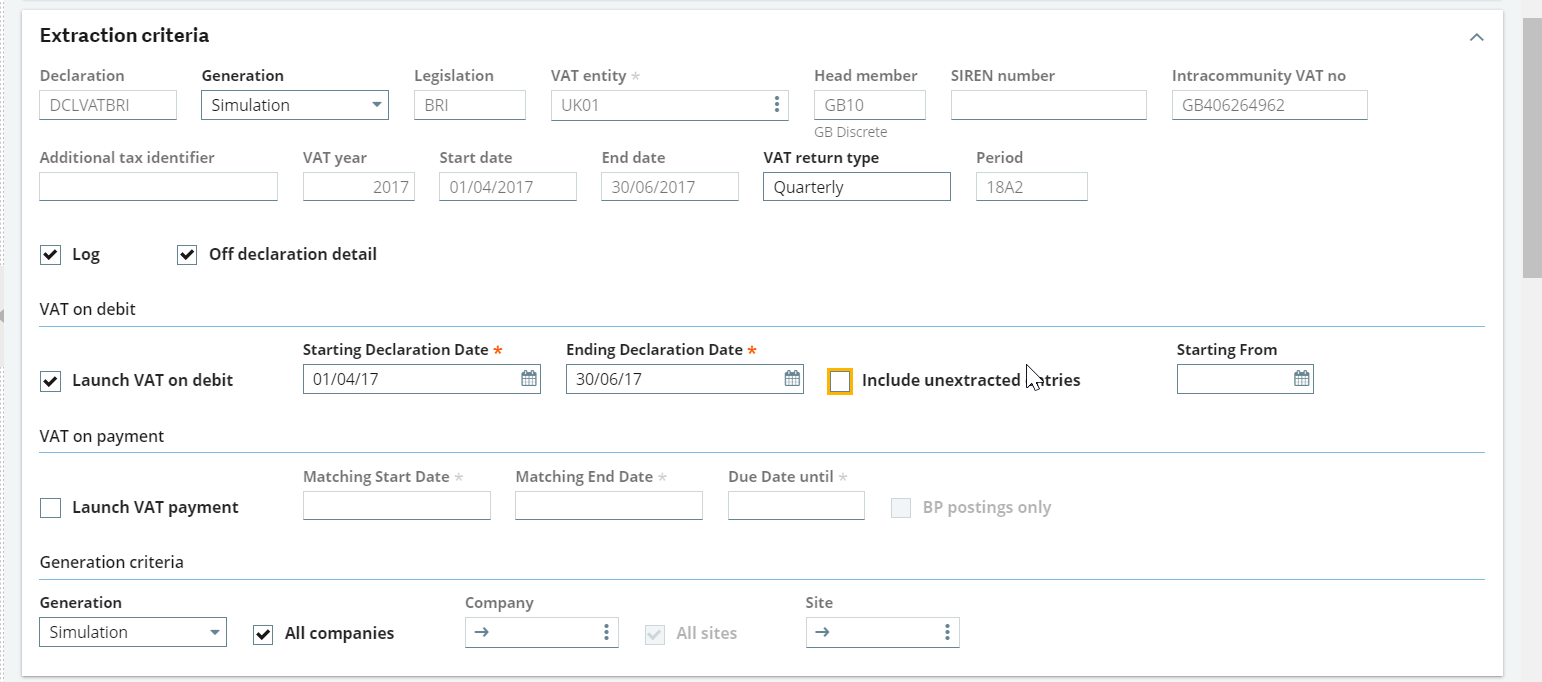

After creating the VAT return using an active VAT form, you need to calculate the VAT amounts in simulation or actual mode.

-

You can simulate as many times you need. Each new simulation deletes former simulations and recalculates the VAT return from the main general ledger according the VAT boxes defined in the VAT boxes function (GESVTB).

-

You must generate in actual mode at least once before you can validate and submit to HMRC. Actual mode marks the journal entries lines that are included in the VAT return. This process is irreversible. Each new actual run extracts the journal entry lines that have not yet been marked.

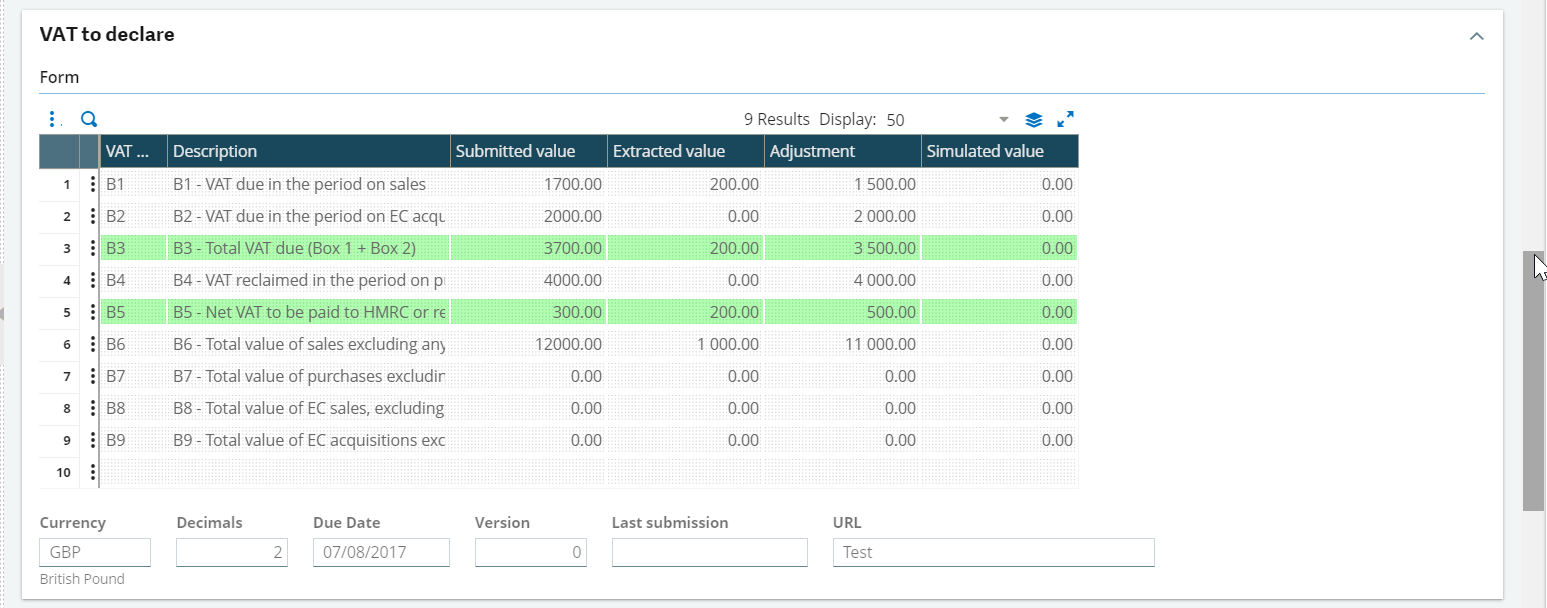

For VAT entities, or company groups, you can view the subtotals per company in the Detail by company grid. The VAT to declare grid displays values for the VAT entity when you run the extraction in actual mode.

You can adjust the VAT return for the VAT entity or per company. Adjustments are permitted by the UK regulation but under certain conditions. Check with HMRC if you are unsure. You can enter adjustments manually, but they do not change the extracted values. Adjustments are included in the submitted value.

From the VAT return, you can access transactions and print reports that include the VAT return or detailed transactions for each extraction.

When you are satisfied with the extraction results and any adjustments, you can validate the VAT return.

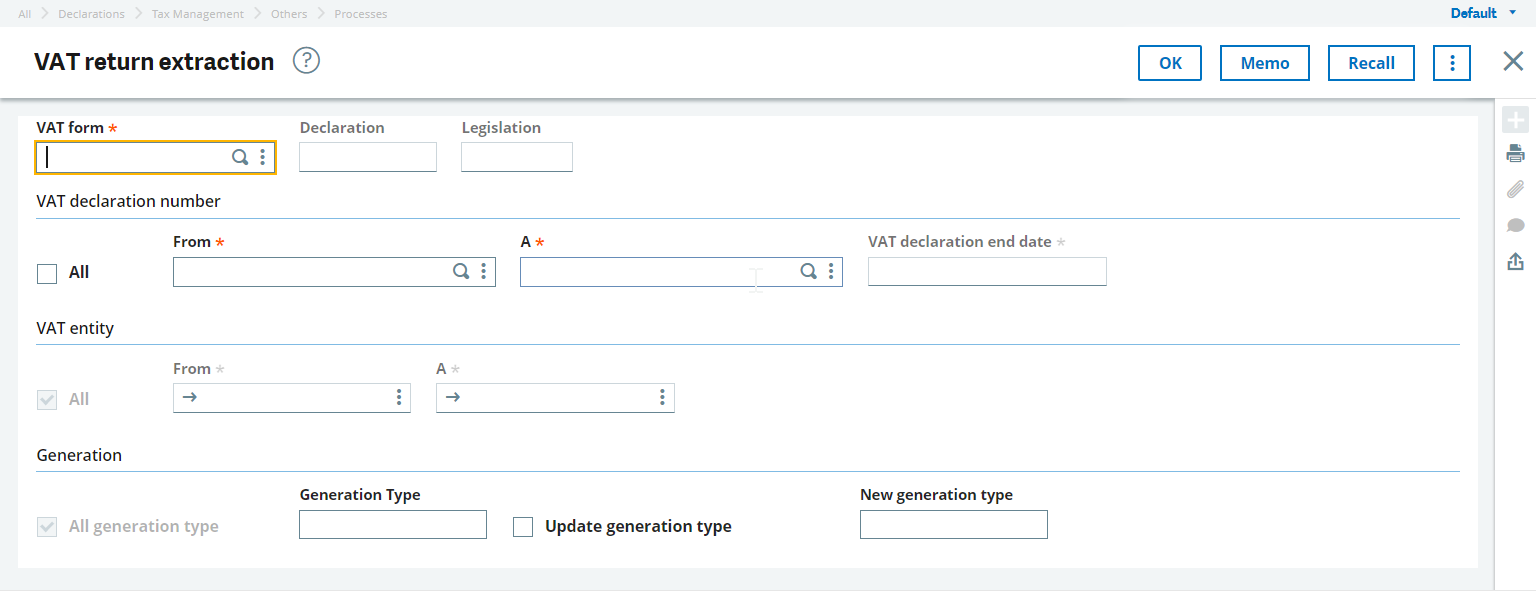

Batch calculations (VFECLC)

Open: DECLARATIONS > Tax management > Others > Processes > VAT return extraction

Use this function to calculate and extract multiple VAT returns. For a given VAT form, you can select one or several existing VAT returns for one or several VAT entities. You cannot extract for an offline VAT return.

After running the extraction, a detailed log file displays relevant information including the Query no., which can be viewed in the VAT returns function.