Fixed assets module

Lease

The following settings are required.

Lease contracts (GESLEA): The rule needs to account for a debt contracted for the lease, with the long–term debt and the short–term debt. Usually, the due date for the short–term debt cannot exceed 12 months.

Generation of fee events (LEAPAY): In the journal entry of the contract installment, you must include the interest expenses. In addition, for the journal entry of the contract installment, there must be an additional journal entry each year, coinciding with the date in which the lease contract was signed.

Debt reclassification: At the end of each year, the installments that must be paid the next year must be moved from the long–term debt account to the short–term debt account.

Accounting

This section describes journal entries associated with fixed assets.

Create the lease contract

- Entry type: LEACRTSPA

- Currently, the following journal entry (LEACRT) is created:

Account

Concept

Debit

Credit

218

Fixed asset

€35,000

174

Long–term financial lease creditors

€35,000

The Spanish rule specifies that the debt, in this example €35,000,) must be split between the long–term and short–term debts. Of the €35,000, the repaid capital in the first year is €7,000. The journal entry should be as follows:

|

Account |

Concept |

Debit |

Credit |

|---|---|---|---|

|

218 |

Fixed asset |

€35,000 |

|

|

174 |

Long term financial lease creditors |

|

€28,000 |

|

524 |

Short term financial lease creditors |

|

€7,000 |

Contract installment

- Entry type: LEAPAYSPA

- Group entry: LPGSP

- Automatic journal: LEPAY and LPSPA

- The Spanish rule indicates that the payment must be split between capital and interest.

Account

Concept

Debit

Credit

524

Short term financial lease creditors

€700

662

Expenses interest

€300

4109

Invoices pending receipt

€1,000

In addition, when the payment is in the same year when the lease contract was created, you must reclassify the debt from long term to short term according to the debt to pay the next year.

|

Account |

Concept |

Debit |

Credit |

|---|---|---|---|

|

524 |

Short term financial lease creditors |

|

€8,400 |

|

174 |

Short term financial lease creditors |

€8,400 |

|

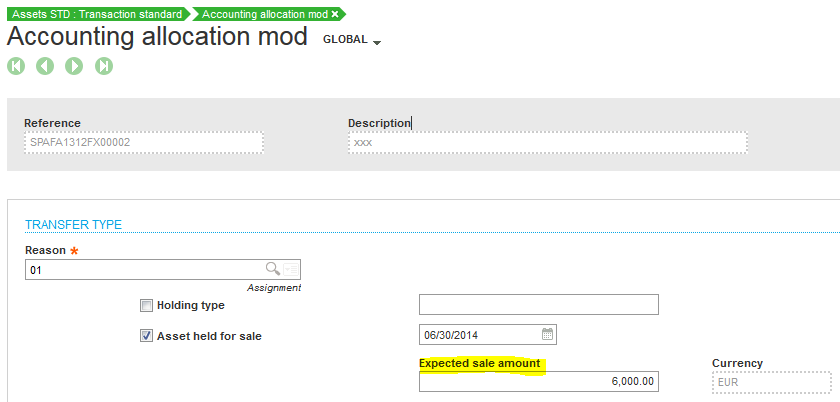

Classification for sale

To comply with accounting requirements, you can enter the expected sale amount in the corresponding field.

Next entry types: FASHELDSALIAS and FASISSIASSPA

At the time of the reclassification:

|

Account |

Concept |

Debit |

Credit |

|---|---|---|---|

|

2813 |

Accumulated depreciation of machinery |

€6,000 |

|

|

691 |

Impairment losses of machinery |

€800 |

|

|

580 |

Non–current assets held for sale (€4,000 – €800) |

€3,200 |

|

|

213 |

Machinery |

|

€10,000 |

At the time of the sales invoice

|

Account |

Concept |

Debit |

Credit |

|---|---|---|---|

|

4300 |

Customers |

€3,630 |

|

|

6711 |

Losses from the non–current assets held for sale(or Gains in the 7711 account) |

€200 |

|

|

580 |

Non–current assets held for sale (€4,000 – €800) |

|

€3,200 |

|

477 |

Machinery |

|

€630 |

Subsidies

Create a subsidy

The following settings are required:

- In the GRTTAXCPY – Corporate income tax % parameter (AAS chapter, GRT group), enter the percent for the corporate income tax at the company level.

- Accounting code: Add lines 6 and 7 to define the required accounts in the journal entry.

- There is an automatic journal: GCSPA.

- There is an account posting type: GRTCRTSPA.

- There is a treatment to calculate the tax amount (corporate income tax): TRTFASSPA routine CAL_IS1.

- There is an automatic journal group: GRCSP. This group is assigned to the previous account posting type. This group is assigned to 2 automatic journals, the GRCRT automatic journal and the GCSPA automatic journal.

Entries when a subsidy is created:

- Automatic journal entry (GRCRT): Journal entry for obtaining the subsidy.

Account

Concept

Debit

Credit

4708

Public entities. Receivable grants (€300,000 * 0.6)

€180,000

6711

Income from government capital grants

€180,000

- Journal entry for the recognition of the deferred tax liability:

Account

Concept

Debit

Credit

8301

Deferred tax (€180.000 * 0.3)

€54,000

4790

Liabilities arising from taxable temporary differences

€54,000

Subsidy depreciation

- There is an automatic journal: GRSPA.

- There is an account posting type: GRTCRBSPA.

- The treatment to calculate the tax amount (corporate income tax) is: TRTFASSPA routine CAL_IS2.

- There is an automatic journal group: GRRSP. This group is assigned to the previous account posting type. This group will be assigned to two automatic journals: the GRREP automatic journal and the GRSPA automatic journal.

- Entries at the depreciation of a subsidy:

- The imputation to the results of the part of the subsidy that corresponds to the depreciation. The standard journal entry is GRREP.

Account

Concept

Debit

Credit

8400

Transfer of government capital grants (€50,000 * 0.6)

€30,000

7460

Capital grants, donations and bequests taken to income

€30,000

- The imputation to the results of the part of the subsidy that corresponds to the depreciation. The standard journal entry is GRREP.

- Journal entry that cancels part of the deferred tax liability:

Account

Concept

Debit

Credit

8301

Deferred tax (€30.000 * 0.3)

€9,000

7460

Liabilities arising from taxable temporary differences

€9,000